It is no secret that the Canadian housing market is running extremely hot. Now more so than ever before. Housing prices have risen, housing starts have risen, the number of transactions has risen. Almost all statistics when looking at houses have risen to levels not seen before. This rise has even been experienced in more rural centers when houses are frequently being bid up, and sold way above the asking price.

There are many factors that have gone into the “booming” (bubble might be more accurate) housing market. Supply change shortages of materials, low interest rates, and stimulus are probably the big three.

Before getting into the rest of the article, if you enjoy our weekly content click the follow button. Also if you could like this post and comment down below it would be much appreciated. This helps us to know that our advice and perspective is valued. Thanks!

Current Housing Market

As mentioned above, the housing market in Canada is at never before seen levels. As of April 2021, the average house in Canada sold for $695,500. That is a year-over-year increase of 42% from April 2020. The number of houses selling has also increased markedly with more than 74,000 houses being sold in April of 2021. For a staggering year-over-year increase from April 2020 of 258%.

The price of a new home in Canada also rose by 1.9% in April compared to March. Year-over-year that increase is at 9.9%. With demand at historic levels despite the continually rising cost of building materials. This increase is the largest increase since February of 2007 less than 1 year before the financial crisis which saw housing prices get decimated.

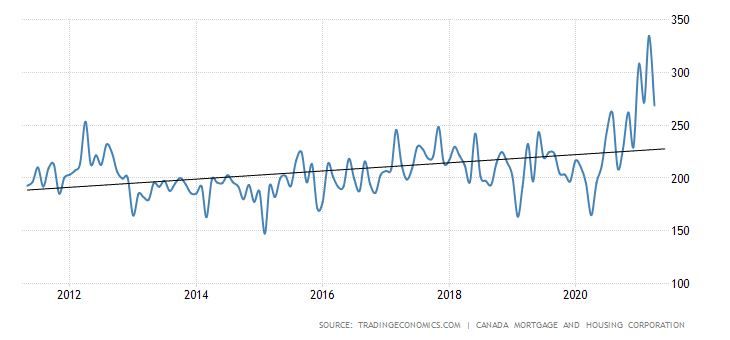

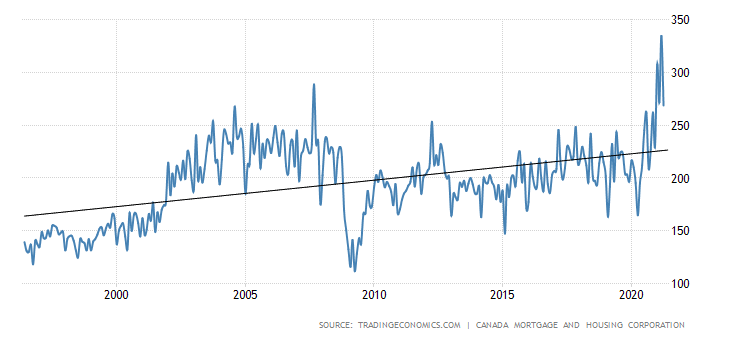

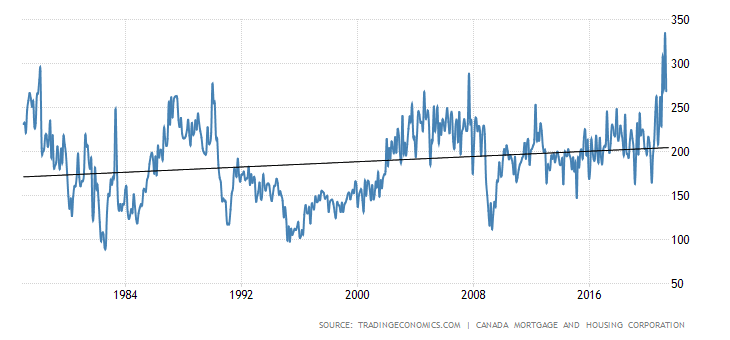

Housing starts, a stat that shows the number of new residential construction projects that began in a month, is also above historical averages. April saw a month over month decrease of 19.8% and currently sits at roughly 268,500. This was below expectations of 280,000 which would still have been a decrease of 16%.

Even with what seems like a drastic decrease, we are still significantly above historic figures. Below is a graph showing housing starts over the last 25 years, with the monthly average below 200,000:

If we look at the current trends, we are sitting above the 5-year, 10-year, 25-year, and 50-year trend line. See below:

Purchasing a House

Purchasing a house is a big decision in life. For most people it is the single biggest purchase they will ever make. The decision should not be taken lightly, especially now as prices are soaring. Before you buy a house, we would encourage you to read the following posts:

When purchasing a house, you have to put some skin in the game. This means that you will have to provide some sort of value (equity) as a down payment to the bank in order for them to issue your mortgage. This equity can come in many different forms and in many different amounts.

Cash/Accumulated Savings/Proceeds from Sale

Cash is the most basic way to provide a down payment. These funds generally come from either your chequing or savings accounts or from the sale of your previous property. It is important to note that the last 90 days of account statements are considered here. Most financial institutions will want to see statements for the last 90 days. Any deposits out of the ordinary or that are suspiciously large within that period will have to be explained.

This means that the use of “mattress funds” (i.e., unexplained cash) is not permitted. It is best practice to deposit that money and let it “age” for 90 days.

Another source of acceptable cash would be gifts from immediate relatives. However, it has to be very clear that the gift does not need to be repaid.

Non-registered Investments

Non-registered investments could also be used as a source for down payments. However, it is important to remember the taxable nature of your non-registered investments. By liquidating and withdrawing these investments you could be creating a taxable disposition. We would recommend talking to your financial and accounting professionals about the tax consequences prior to proceeding with this option.

RRSP Home Buyers Plan

RRSPs are potentially a great source when purchasing a home. Generally, when you withdraw funds from and RRSP, they are added to your taxable income. That is not the case with the RRSP Home Buyers Plan. We have done a blog post specifically dedicated to this in the past check it out below:

Property Equity

For those that already have equity in a different property, you can leverage that equity to purchase another property. If you have equity in a property and want to buy another property with that equity consult your mortgage lender and financial institution. Because you are buying a property with equity their mortgage rules on the amount you need for a down payment may differ.

First-Time Home Buyers Incentives

The FTHBI is a “shared” mortgage with the government of Canada. For existing homes, they offer up to 5% of the value of the home for a down payment. For new builds, they offer up to 10%. However, the total down payment (your portion plus the FTHBI) cannot exceed 19.99%. This means that all qualifying mortgages must still be insured by CMHC (3% additional charge). Furthermore, any increase in property value upon sale of the house must be shared with the government.

Although this may be a good option for some people, we would recommend that you be cautious. Consult your financial advisor first prior to proceeding.

Unacceptable Down-payment Sources

When it comes to buying a house, there are sources that are not eligible to be used for a down payment. Another name for these sources is non-traditional sources.

Back in June of 2020, Canadian Mortgage and Housing Corp. announced changes to it’s underwriting criteria. In that update, they announced that non-traditional sources of down payment that increase indebtedness will no longer be treated as equity for insurance purposes.

According to CHMC, these non-traditional sources include any source that is arm’s length to and not tied to the purchase or sale of the property such as:

- Borrowed funds,

- Gifts (presumably from non-immediate relatives),

- 100% sweat equity (<50% of minimum required equity is allowed).

- Lender cash back incentives.

Conclusion

The Canadian housing market continues to run hot. People continue to buy and build houses even with prices rising at historic rates. This is happening so much so that houses are often being bought for above their asking price. Sure, their are factors that play into this (interest rates, supply chain breakdowns, stimulus) but what happens when these new owners go to sell in the future? Or what about when they their mortgage term is up in 5 years?

Will interest rates still be just as low then? Will our purchasing power be the same with all the expected inflation coming? It seems people aren’t taking these future considerations into account.

For the time being, all they care about is getting into that new, or at least new to them, house. With higher prices for both materials and houses, people need more money for their down payment and may be looking at sources they previously hadn’t considered. This could be forcing Canadians to have even more of their net worth tied up in real estate than they already had.

We are also on social media now, click the social icons in the top right corner and follow us on Facebook, Instagram, and LinkedIn.

Share your thoughts with us!

If you enjoy the forbeswealthblog content please like, comment, and share it with your friends. Also, click the follow button on the right side to follow our blog for great original content every week.

Visit: www.forbeswealth.ca

Disclaimer: This Forbes Wealth Blog is for informational purposes only and does not constitute financial, legal, or tax advice of any kind. Please consult your legal, accounting, tax, investment, banking, and life insurance professionals to get precise advice relating to your particular situation before acting upon any strategy