2019 has nearly come to an end, with 2020 just around the corner. That means that in less than a month we all get a little more TFSA contribution room! YAY! This new contribution room is available to everyone over 18. In case you don’t already know, here is why you should max out your TFSA.

Before getting into the rest of the article, if you enjoy our weekly content click the follow button. Also if you could like this post and comment down below it would be much appreciated. This helps us to know that our advice and perspective is valued. Thanks!

If after reading this post you would like to read more about TFSA’s, check out A Beginners Guide to The TFSA.

History of TFSAs

Tax Free-Savings accounts started in 2009, and originally had a $5,000 per year contribution limit. Anyone that has a valid social insurance number and is 18 years of age can open a TFSA. Even if you are considered a non-resident in Canada.

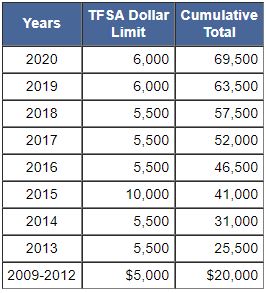

Since their inception, there have been several contribution increases, as is seen in the image below. All contributions and income earned in the account can be withdrawn tax-free at any time.

Unlike RRSPs, TFSA contributions are made with post-tax earning. This means that contributions are NOT eligible for tax deductions.

In 2020, everyone that qualifies for a TFSA will be entitled to an additional $6,000 of contribution room. The maximum that anyone is eligible to contribute is $69,500.

Below you can find a breakdown of contribution room by year:

Or if you would prefer, the chart below shows the eligible contribution room based on year of birth:

A person is entitled to Tax-Free Savings Account contribution room in the year that they turn 18. For example, if someone turned 18 in the 2013 calendar year, they would be entitled to $49,500 as of January 2020.

TFSA contribution room limit is indexed to inflation and rounded to the nearest $500. This is the reason for the increase for the 2019 calendar year. The CRA indexation increase for 2019 was 2.2%, pushing the contribution limit past the rounding point. This indexation process takes place every year.

There is a simple formula to calculate how much contribution room is available for a person at the beginning of each year: Unused TFSA contribution room to date + Withdrawals from previous year + new contribution room.

Warning: make sure you do not over-contribute. Any over-contribution is penalized 1% per month until remedied.

So why should you maximize your TFSA contribution room?

TFSA Withdrawals Can Be Re-contributed

Any withdrawals that are made from a Tax-Free Savings account, can be re-contributed in the following calendar year. Conversely, withdrawals from a Registered Retirement Savings Account (RRSP) cannot be re-contributed and that contribution room is lost.

For example, let us say Bill had maxed out his TFSA contributions in January of 2017 of $52,000. Bill did not contribute to his TFSA in 2018. However, In June of 2018, Bill withdraws $12,000 from his TFSA. Calculating his eligible contribution room for 2020 is done as follows: $5,500 (2018 unused contribution room) + $12,000 (withdrawals in previous year) + $6,000 (2019 contribution room) + $6,000 (2020 contribution room) = $29,500. You can confirm your TFSA contribution room on your CRA profile.

Just to reiterate, withdrawals can be re-contributed but only in the next calendar year, not during the year of withdrawal.

Furthermore, even when gains are withdrawn they can be re-contributed. Let’s say you maxed out your TFSA in 2019 and had lifetime contributions of $63,500. However, your investments have done well and the market value is $80,000.

Near the end of 2019 you decided to upgrade your car and withdrew the full $80,000. In 2020, your contribution room would be $86,000 calculated as follows; $80,000 (previous year withdrawals) + $6,000 (2020 contribution room).

Investment Gains are truly Tax-Free

Although contributions to a TFSA are done with after-tax dollars, all contributed funds grow tax-free forever. Any income that is generated, whether realized or unrealized, will not be taxed while in the TFSA or when it is withdrawn.

Even upon death, the full market value of your TFSA is received by your beneficiary or estate completely exempt from tax.

Contributions/Withdrawals at Any Age or Time

Once a person turns 18 they are eligible for that year’s TFSA contribution limit. Contributions can be made at any time throughout the year (as long as no over-contributions are made) and can be made regardless of age. RRSPs, on the other hand, must be converted to RRIFs at age 71. At age 72, no additional contributions to RRSPs are allowed.

Withdrawals from a TFSA can happen regardless of age or reason and are completely tax-free. If a withdrawal is done from an RRSP, that contribution room is lost, and the withdrawal is claimed as taxable income in the year of withdrawal.

Due to the Tax-Free nature of withdrawals, TFSAs make for great emergency funds. If a large purchase is needed, a withdrawal will not have any tax consequences or push you into the next tax bracket.

We also recommend trying to max out your TFSA as early in the year as possible. This allows the most time for the funds to grow tax-free.

TFSA Withdrawals Do Not Count as Income

Withdrawals from a TFSA, as noted above, are completely tax-free and are not classified as taxable income. However, withdrawals from an RRSP have a minimum amount of tax withholding tax levied at source and the withdrawal amount is added to your taxable income.

Having withdrawals counted towards income is significant and should be carefully watched. During retirement when income surpasses a certain level, clawbacks are triggered on Old Age Security (OAS). Clawbacks to OAS in 2019 are triggered at the $77,580 income level. If net income is higher than $125,937, OAS is completely clawed back and reduced to zero.

Note that there is an exception to the OAS clawback ceiling. For more information on that here is a great article written by one of our colleagues Aaron Hector: OAS Clawback Secrets for the High-Net-Worth.

Conclusion

For most client situations TFSAs are the most tax advantageous savings vehicle available. They offer the most flexibility with regards to unexpected withdrawals, and don’t leave investors in an uncomfortable income tax position when they need the money the most.

If you would like more information on TFSAs or if you’re interested in starting to save, send us a message. You can use the chat function in the bottom right corner, or you can fill out our Contact Form. It would be our pleasure to get to know you and your financial situation better.

Note: This is an updated version of 4 Reasons to Max Out Your TFSA.

We are also on social media now, click the social icons in the top right corner and follow us on Facebook, Instagram, and LinkedIn.

Share your thoughts with us!

If you enjoy the forbeswealthblog content please like, comment, and share it with your friends. Also, click the follow button on the right side to follow our blog for great original content every week.

Visit: www.forbeswealth.ca

Disclaimer: This Forbes Wealth Blog is for informational purposes only and does not constitute financial, legal, or tax advice of any kind. Please consult your legal, accounting, tax, investment, banking, and life insurance professionals to get precise advice relating to your particular situation before acting upon any strategy