“Canadian Average Debt Load now up to $22,081, 3.6% rise since last year”

“Canadian Household Debt reaches $1.8 Trillion…”

“Canadian Consumer Debt Just Keeps Growing”

These are just a few of the alarming headings that we see showing up in the mainstream press on a more frequent basis. But how much validity is there behind these statements, or are they purely just shock and awe?

Before we go into more depth it is important to define Consumer Debt and Household Debt.

According to Investopedia, Consumer and Household Debt consists of debts that are owed as a result of purchasing goods that are consumable and do not appreciate. “Consumer debt” is a term often used alongside “household debt” as both are often connected with credit cards, mortgages, auto loans, and payday loans.

If you look at the cost of living and housing across the country, it’s not surprising that consumer debt is up, especially if mortgages are included. The rise of consumer debt is not positive, but is not the problem in and of itself.

Generally speaking, the monetary value of the debt an individual carries increases as they earn more and generate more wealth. We like to call this the debt to equity ratio. As long as debt to equity ratios remain healthy – more equity than debt – we can view this a a sign of positive growth. However, when we compare national debt figures to national GDP figures, they paint a less than ideal picture.

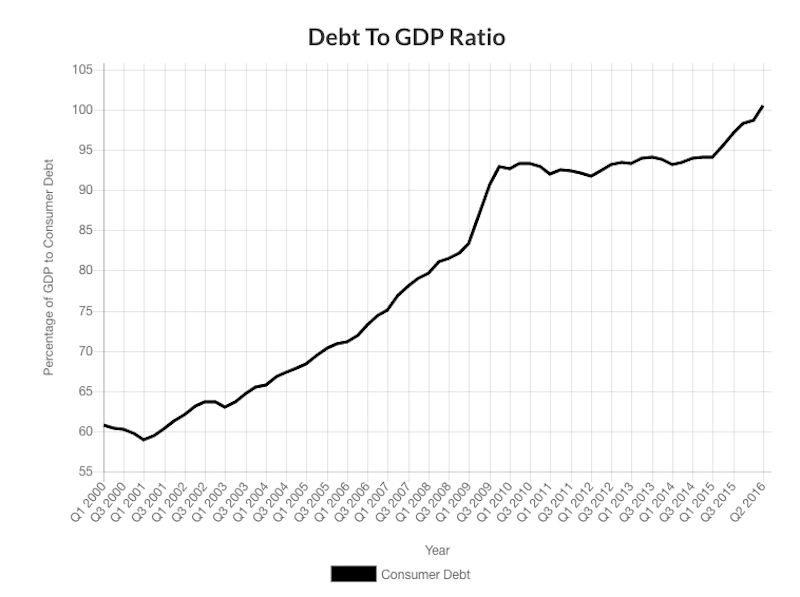

In 2005, Canadian GDP was $1.169 Trillion USD. The 2005 household debt vs. GDP ratio was 68.33973. Fast-forward to 2017 where Canadian GDP had grown to $1.529 Trillion. This seems like a substantial increase but not when compared to the increase in household debt, which in early 2018, hit $1.8 Trillion. In 2017, the household debt vs. GDP ratio was 101.15343.

Even more unnerving is the household debt vs. disposable income ratio, which in January of 2018 was 172.62%.

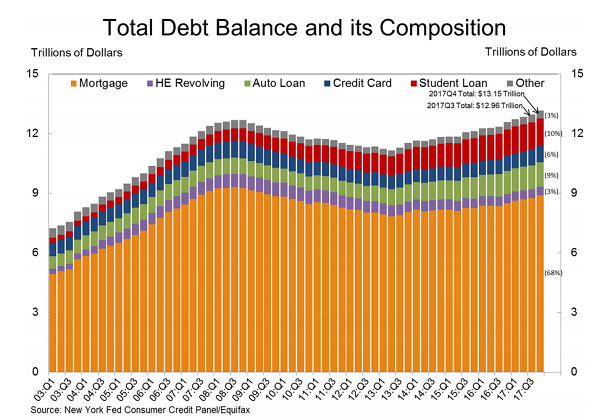

The largest portion of household debt is mortgages. However, there are 3 other categories that contribute large sums to the household debt figure; Auto Loans, Credit Cards, and Student Loans.

Here is a graph showing household loan breakdown for the USA:

Although the above graph is for the USA, it is safe to assume that the Canadian economy would be represented similarly.

Surprisingly, credit cards seem like a minor issue, making up about 6% of total household debt. However, they are one of the easiest forms of debt to misuse and can easily compound into astronomical outstanding balances.

The average Canadian household has about $4,000 in credit card debt. This doesn’t sound that bad, but credit cards have massive interest rates, some reaching into the high teens (19%).

Not only is credit card debt increasing across Canada, but growing mortgages and student loans are also a large cause for concern. Read our previous posts on mortgages and the housing market by clicking here and here.

We are not suggesting you avoid credit cards all together. They have many added benefits (i.e., ease of use, reward programs, building a credit score), but view them as a cash flow tool, ensuring the balance is paid in full at every month’s end.

If you enjoyed this article please like, comment, and share it with your friends. Also, follow our blog for great original content every week.

Visit: www.forbeswealth.ca

Disclaimer: This Forbes Wealth Blog is for informational purposes only and does not constitute financial, legal, or tax advice of any kind. Please consult your legal, accounting, tax, investment, banking, and life insurance professionals to get precise advice relating to your particular situation before acting upon any strategy.

Read more: Consumer Debt https://www.investopedia.com/terms/c/consumer-debt.asp#ixzz5BdkrujwY

http://www.cbc.ca/news/business/equifax-debt-loads-1.3884993

http://www.cbc.ca/news/business/canada-credit-cards-transunion-1.4015250

The average Canadian owes $8,500 in consumer debt, excluding their mortgage: Ipsos poll

https://fred.stlouisfed.org/series/HDTGPDCAQ163N

https://tradingeconomics.com/canada/households-debt-to-income

Who knew? Canadians’ alarming household debt levels may actually be conservative

Canadian household debt hits $1.8 trillion as global watchdog warns of risks to economy

Canadian consumer debt just keeps growing — but here’s why it’s not a problem yet