At a recent social event, a gentleman who was close to retirement was commenting that it was no use attempting to save money with current interest rates so low. “Besides, the government will look after me in retirement” he claimed.

We thought it would be useful to analyze his situation for this blog post.

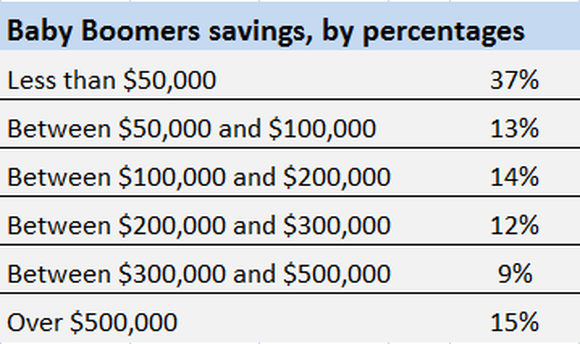

Unfortunately, he is not alone. Many baby boomers have minimal retirement savings. As the graph below points out, 50% have accumulated less than $100,000 in the way of retirement savings, and are likely to be at least partially dependent on the government for lifestyle expenditures in retirement.

Data Source: PWC Employee Financial Wellness Survery

More worrisome, over a third of baby boomers have saved less than $50,000 for retirement, and just 15% have accumulated nest eggs north of $500,000. These figures suggest a significant proportion of baby boomers could end up struggling to pay their bills in retirement.

With reasonable rates of return, a retiree with $500,000 beginning to take an income of $2500-$3000/mon from savings at age 65, should have enough assets to maintain the same monthly spending into their 90s.

For Pensions, the Manitoba Pension Commission has imposed rules limiting maximum withdrawals to 6% annually from a regulated pension account. They enforce a maximum withdrawal rate so the account will provide an income to age 90.

Of course, most people live beyond 90 which is why financial planners often recommend a 4% withdrawal so savings will last until age 100. At a 4% rate, the baby boomers with accounts smaller than $100,000 will produce less than $4,000 in annual retirement income. This means that 50% of the retiree population produces less than $4000 retirement income per year above government benefits.

For the purpose of this case study, let us assume the gentleman described above is named Bob. Bob is age 58, earns $40,000 salary per year and has no retirement savings. In other words, he lives “paycheck to paycheck” on his net income of $2,500 per month.

As retirement approaches quickly for Bob, it is crucial that he uses his last 7 working years to save as much as possible unless he is preparing himself for a significant drop in income.

Factoring in Canada Pension Plan (CPP) and Old Age Security (OAS) benefits, Bob’s base retirement income will be about $1,590 per month. This amount accounts for only 55% of the $2,860 ($2,500 indexed 7 years into the future) of lifestyle expenses Bob is used to receiving.

- Bob’s maximum CPP entitlement at age 65 will be $920 per month.

- The OAS at age 65 is projected to be $670 per month.

Of course, the government does provide additional financial support for low-income Canadians in the form of a Guaranteed Income Supplement. However, Bob will not receive any Guaranteed Income Supplement. He has already received more than the maximum income cutoff of $1,482 per month as a single person, or $1,960 as a married couple.

If Bob wanted to maintain his current lifestyle expenditures, he would need additional savings of $254,000 at a 6.0% rate of return to generate the extra $1,270 per month to supplement CPP & OAS benefits.

A retirement fund of $500,000 would add an extra $2,500 per month. In addition to the $1590 indicated above (CPP & OAS), retirees will only have a little over $4,000 per month before taxes. Married couples could factor in their spouse’s OAS and CPP entitlement to the household income.

If Bob decides to retire early at age 60, he is penalized with CPP being reduced to 64% of the full entitlement he would have otherwise received at age 65. In this case, his CPP would only be $388 per month. Early retirement is almost out of the question for Bob.

If for health reasons, Bob becomes totally disabled in the next 7 years, he would lose his employment income but a CPP disability benefit of up to $975 per month (adjusted for earnings history) could be applied. With no other sources of income until age 65 when Bob would receive OAS, this scenario would leave Bob to cut his lifestyle expenses severely. He may have a hard time making ends meet.

We have outlined a fairly dramatic example, but this is the reality for a lot of Canadians who haven’t planned ahead. If you have any questions about what your retirement income situation could look like, please contact us!

We would love to hear your thoughts, so leave us a comment, like this post, and share it with your friends. Follow our blog for more great content in the future.

Some additional articles of interest on the subject:

https://www.fool.com/retirement/2016/12/17/baby-boomers-average-savings-for-retirement.aspx

Disclaimer: This Forbes Wealth Blog is for informational purposes only and does not constitute financial, legal, or tax advice of any kind. Please consult your legal, accounting, tax, investment, banking, and life insurance professionals to get precise advice relating to your particular situation before acting upon any strategy.