In today’s society, debt is inevitable for most. At some point in our lives, we will shoulder debt in one form or another (i.e., mortgage, car loan, student loan, a line of credit, credit card). With debt there is also interest, with rates and cost are dependent on a lot of variables (i.e., credit rating, amount, type of loan, lending institution, etc.).

The standard retail level interest rates are dependent on the “Prime Rate” (if you are not familiar with this term or would like to learn more click here). A familiar term is prime plus 2%, which means that the borrowing rate would be prime (3.45%) plus an additional 2%, or 5.45%. For more information about the pros and cons about rising interest rates, we will leave links at the end of this article.

Paying down debt is a very common excuse for a lot of people when pressed for why they aren’t saving for the future. Sounds logical that paying off debt should be your number one priority. Let’s look at some facts about our Canadian society and it’s debt.

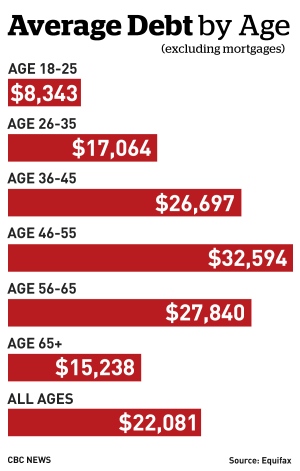

If we look at recent consumer debt history, the figures are astonishing. In Q3 of 2016, the average Canadian consumer debt per person was $22,081. Up 3.6% from only 1 year prior. This large chunk of debt fails to include one of the largest categories of debt – mortgages.

Here’s a chart breaking down consumer debt by age per person:

A break down of consumer debt by province:

Not only are people carrying more debt now than in recent history, the ratio between debt and disposable income has reached record highs in Canada. In Q2 of 2017, credit market debt as a proportion of household disposable income increased to 167.8%.

Paying off debt quickly seems logical when we take these numbers and recent trends into account. However, that might not always be the wisest thing to do from a long-term financial perspective.

First, let’s look at the returns that are can be generated on an investment account. For example, we could say the average market return is 6%. This means if $100,000 dollars is invested today, in one year you would have $106,000. Assuming a 6% annual return, the investment will double in value about every 10-11 years.

When you pay off debt, think of the interest on the debt accumulating as a negative return. If the loan is $100,000 with 5.45% interest and you paid off the $100,000 you just received an -5.45% annual loss.

Most loans, however, do not have interest rates that high. For instance, the interest rate on a mortgage would be somewhere between 2.5% – 4% generally.

Here is a potential example:

Bob just got a large bonus at the end of the year of $15,000, but he’s unsure of what to do with it; use it for the mortgage or invest it? Well, let’s assume the interest on Bob’s mortgage is 3.45%. If he puts the full $15,000 towards the mortgage he just saved that 3.45% worth of interest owing on that chunk of money. On the other hand, if he invested the $15,000, and the market performs at its average rate of +6%, Bob would be further ahead by +2.55%.

At 3.45% interest, Bob could save himself $517.50 by putting his money towards the mortgage. With a 6% investment return his $15,000 investment would have generated $900 in one year. If the money is left in the investment account for multiple years, compounding interest starts to play a significant role (more info on compounding interest here).

With a loan that has an interest rate at 5% or lower, it would be worthwhile weighing the option of making just minimum payments on the loan and investing the surplus cash flow that would’ve gone towards paying down the loan. Even with a 5% interest rate you are still +1% further ahead if the market performs at its average of 6%.

The other point to consider is how you achieve that 6% long-term rate of return. Participating in fixed income and equity market investing can be volatile; meaning returns will vary from year to year. To achieve a long-term average of 6% there will be years of +10% and years of 0% or even negative returns.

The return that is generated on an investment is only as good as the advice you receive and investment you pick. So, be diligent in searching for a financial advisor and working with them to find suitable investments for your particular situation that also fit your risk tolerance and time horizon.

Investing rather than paying off debt (even if it has a low-interest rate) is not for everyone. It depends on comfort level and ability to deal with the emotional and cash flow burden of carrying debt for an extended period of time.

If you need help figuring out your situation fill out our contact form here, and we will get back to as quickly as possible. Or if you would like more information on our company visit our website https://forbeswealth.ca.

We would love to hear your thoughts so leave us a comment. Like our post and follow our blog for more great original content in the future.

The Pros of rising interest rates

The Cons of rising Interest rates

Sources:

http://www.cbc.ca/news/business/equifax-debt-loads-1.3884993

Disclaimer: This Forbes Wealth Blog is for informational purposes only and does not constitute financial, legal, or tax advice of any kind. Please consult your legal, accounting, tax, investment, banking, and life insurance professionals to get precise advice relating to your particular situation before acting upon any strategy.