The 1920’s were the wild west when it came to individuals investing in the stock market. Regulations were almost non-existent. Almost anything and everything could be said when promoting individual stocks. It was truly buyer beware.

This supported a tremendous buying spree which came to a screeching halt in November of 1929. In the following 5 years the market declined an astonishing 90%.

Below is a chart showing the rise and then sudden crash of the stock market from 1920-1936:

This critical decline put the government in a situation where they were forced to “do something”. In 1934 the US introduced the Securities Exchange Commission to regulate the market. Included in the regulation was the legal framework for the creation of mutual funds.

While there were a few mutual funds that were formed following the creation of the 1934 legal framework, the concept was not used to it’s fullest potential for decades. Individuals did not trust the stock market due to the significant loses in the early 30’s, which saw the economy fall into one of the worst recessions in history.

However, the 1980’s and 1990’s were the golden era for mutual funds. With the increased demand, the number of mutual funds being put to market seemingly exploded. Mutual funds became an easy, convenient, and cost effective way to participate in the stock market, and provided professional oversight on individual stock selection by a portfolio manager.

Currently, in Canada when you add up all the different mutual funds including their different series for different taxable situations, you have in excess of 25,000 series of funds. In 2015 it was estimated that 33% of Canadian households held mutual funds. By the end of 2017 the total assets held in mutual funds was $1.48 Trillion.

Researchers with a keen eye noticed that the rate of return for the average mutual fund did not exceed the return of the respective index they were tracking. The index is often referred to the weighted average of group of stocks on a particular market

Due to the reality that a lot of mutual funds didn’t seem to add any value above and beyond the rate of return for their respective index, ETFs or Exchange-traded Funds started to make their ascent.

If you can eliminate the use of professional portfolio managers, you can offer a substantially cheaper product while still providing an average rate of return which matches the index.

To operate an ETF you only need a few accounting staff to ensure that enough securities are bought and sold on a daily basis to align the ETFs holdings with the same securities weightings of the associated index. This keeps your costs very low, and in turn you can pass on the savings to the end investor.

Although being created over 20 years ago, ETFs have only began to appeal to the average investor in recent times. The average higher cost mutual fund and its lackluster performance was brushed aside for low-fee no-mess ETFs, and why not? They performed the same.

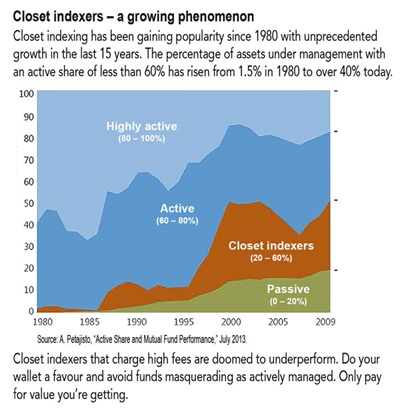

Passive investing (or index investing) aims to track a desired index as closely as possible by matching the index’s weighting of securities. ETF’s definitely fall into this category. However, there are also a number of mutual funds that employ professional managers but simply follow the index as “closet indexers”. While there are no official numbers, we suspect as many as 40% – 50% of funds available today follow a passive mandate, whether intentional or not.

What about the other side of the investing spectrum? What about the highly active managers?

Highly active investment managers or active share managers will invest in stocks, bonds, and other securities in order to generate a return. The highly active share manager aims to employ brain power and keen decision making on specific securities to consistently out perform an index.

Often times highly active managers will hold portfolios that have almost no overlap with the weighting of securities on the index which they are compared to. At other times their portfolios may look very similar to the index with a lot of overlap.

It really depends on the business cycle, interest rates, political policies, and consumer trends. As each of the above criteria change, so do specific businesses, entire industries, and geographical regions.

Active managers seek to add value by continually analyzing these factors and making decisions to move in and out of specific securities to avoid downside, where a passive strategy would just stay fully invested and weather the storm.

I have included a chart that compares active share investing to passive investing below:

We would love to hear your thoughts, so leave us a comment, like this post and share it with your friends. Follow our blog for more great original content in the future.

For more information on…

Mutual Funds: Click Here,

ETF (Exchange-Traded Funds): Click Here,

Closet indexing: Click Here,

Passive Vs. Active Investing: Click Here and

Forbes Wealth Management: Click Here.

Sources:

http://www.howtotradestocks.org/blog/1930s-and-2008-crash-comparison/

Disclaimer: This Forbes Wealth Blog is for informational purposes only and does not constitute financial, legal, or tax advice of any kind. Please consult your legal, accounting, tax, investment, banking, and life insurance professionals to get precise advice relating to your particular situation before acting upon any strategy.