As some of you may have noticed, we took a short break from our weekly blog for the warm summer months. We are now back to business as usual and will be posting regularly.

Picking up where we left off, we previously released a couple posts shedding light on the crippling effect of the Canadian Debt situation. To recap, household debt has reached all-time highs and appears like it will continue at this pace for the foreseeable future (see our post on credit cards/consumer debt and auto loan delinquencies).

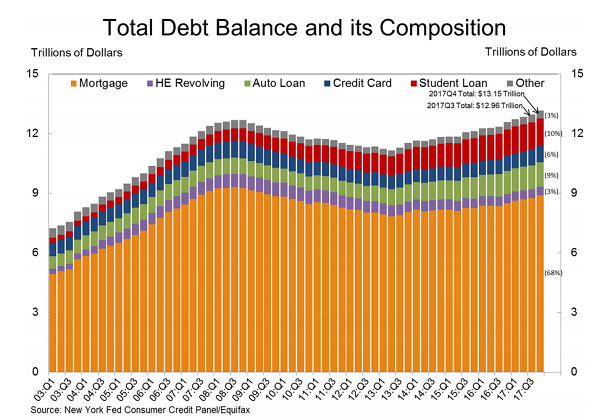

It is surprising how big of a role student debt plays in the composition of national debt. Canadian student loans now make up roughly 10% of the national household debt.

Canadian students owe $28 Billion to the government for student loans. This figure only includes provincial and federal student loans. Many students have gone other routes to obtain financing, often banks or parents, which are not included in the valuation.

The average Canadian student graduates with roughly $27,000 of debt, with a repayment plan set for 10 years. The Government of Canada’s federal student aid program has interest rates of 5.95%., with interest beginning to accumulate the month following graduation and payments starting 6 months after graduation.

Assuming a student graduates with $25,000 of debt and plans to pay it off over the 10 years with 5.95% interest they will have paid $12,500 in interest alone. This is also assuming that the interest rates stay constant.

Graduation is a hectic time for students; getting a full-time job and establishing a career, finding a permanent place to live, and having more bills to pay. These “real world” focuses tend to derail student loan repayment priorities and often cause regret for past graduates. 77% of graduates under 40 said they regret the way they spent money while in school.

Over the last decade, tuition costs have increased by nearly 2.5% year over year. In 2007-2008 a 4-year degree at a private institution would have cost $27,520. Now in 2018, the average cost is about $34,740. That is a $7,220 increase in 10 years.

At a public institution, the increase over the same time span has been nearly 3.25%. Jumping from $7,280 to $9,970.

When looking at the reason most people decide to pursue post-secondary school (to maintain a decent quality of life), it seems ironic that they are often set so far back because of the cost of financing.

What, at one point, seemed like the ideal life path (going to university to get further in life), is now causing many negative side effects. Many graduates are forced to delay important milestones until much later in life.

The average age of marriage has been pushed off later in life and has increased by nearly 3 years since 2000 (see historical marriage ages). Student loans are not the only factor at play here, but financial security definitely plays a part in marriage and relationships (see why it’s important to talk about money).

The average first time home buyer is also in their late 20’s (about 29). This means that a large segment of graduates and millennial’s are forced to move back in with their parents or rent for a substantially longer time due to the inability to make a down-payment.

With the student debt burden beginning to affect more people, many have decided to stand up against astronomical university and financing costs. The Canadian Federation of Students has taken steps to try and combat these issues. In doing so they have created a petition to get interest rates on student loans removed.

If you’re a recent university graduate with a sizeable student loan and want to plan ahead, or if you’re a concerned parent or grandparent looking at how you can help plan ahead for your children’s financial future, please reach out and get our opinion.

Share your thoughts with us!

If you enjoyed this article please like, comment, and share it with your friends. Also, follow our blog for great original content every week.

Visit: www.forbeswealth.ca

Disclaimer: This Forbes Wealth Blog is for informational purposes only and does not constitute financial, legal, or tax advice of any kind. Please consult your legal, accounting, tax, investment, banking, and life insurance professionals to get precise advice relating to your particular situation before acting upon any strategy.

Sources:

Student debt: The crippling side effect of education

77% of Canadian graduates have regrets about student debt: poll

https://trends.collegeboard.org/college-pricing/figures-tables/tuition-fees-room-and-board-over-time

http://zillow.mediaroom.com/2015-08-17-Todays-First-Time-Homebuyers-Older-More-Often-Single

Canadian students owe $28B in government loans, some want feds to stop charging interest